Q1 2026 | Geopolitics as a Structural Variable

By Nicholas Lebuis

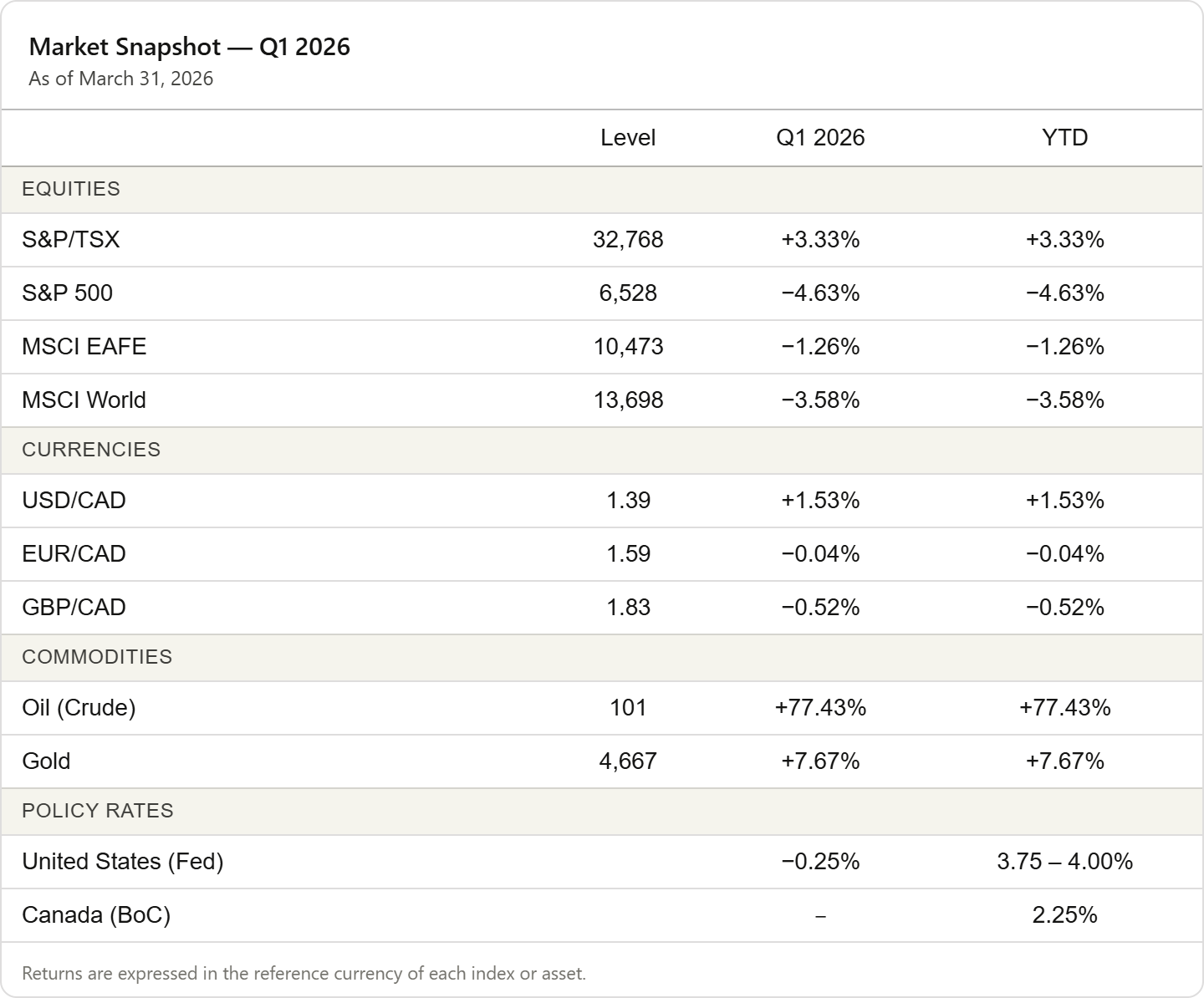

The first quarter of 2026 marked a shift in investor complacency toward geopolitical risk. The prolonged closure of the Strait of Hormuz and escalating tensions in the Middle East have transformed risk premiums from a theoretical exercise into a tangible reality. Crude oil has crossed critical thresholds, forcing a divergence between indices: while the S&P 500 retreated by approximately 4.6%, the S&P/TSX rose over 3.3%, supported by its energy component.

The Shift: Re-evaluating Rate Expectations

The defining characteristic of this quarter is a breakdown in correlation. We are witnessing a “re-regionalization” of performance. The retreat in US indices was driven not only by shifting interest rate expectations but also by a correction in the technology sector, which had reached historically high concentrations. Passive allocations heavily weighted in these areas face headwinds that geographical and sectoral diversification—specifically energy, resources, and gold—effectively offset.

The Role of Alternatives

In a “Higher for Longer” environment, the value of macro judgment outweighs broad exposure to market beta. In this context of uncertainty, private credit and real assets merit attention for their long-term expected returns and their alignment with a disciplined investment horizon. As public market volatility persists, the illiquidity premium of private markets serves as a structural tool for investors seeking to align capital with long-term objectives.

Conclusion

The quarter serves as a reminder that liquidity has a price and that geopolitics remains a primary architect of global markets. In an era of systemic uncertainty, the structure of capital is the foundation of permanence.

Stay Informed

Bloomridge publishes a limited number of articles each year. Distribution is limited.